Probably in light of the controversies that emerged upon reading the first drafts (see also the contribution by Luigi Belluzzo in Il Sole 24 Ore of August 8 on page 3), the press release from Palazzo Chigi has limited the effective date of the amendment, expressly indicating that the increase will apply to individuals who transfer their tax residence to Italy after the date of entry into force of the decree. The Minister of Economy and Finance, Mr Giancarlo Giorgetti, during the press conference yesterday, stated that it is “very difficult to assess” how many new tax residents have reinvested in Italy, emphasizing that “We are against inaugurating a season of competition to create favorable tax situations for individuals and businesses. If this competition starts, countries like Italy, which have very limited fiscal space, are inevitably destined to lose.” There have been, of course, speculations about these statements and the possible external pressure against the regime applicable to new tax residents in Italy.

That said, here is a summary of what we know and the practical effects of this questionable adjustment:

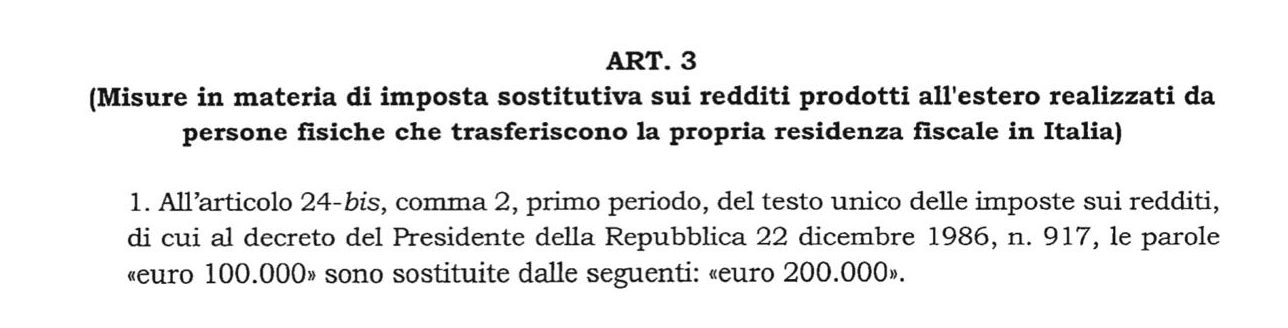

- Those who have already entered the new residents’ regime and paid 100,000 euros last June for the 2023 tax year should reasonably maintain this tax for subsequent years. We will continue to monitor the situation, and an official position by the Ministry of Economy and Finance and/or the Director of the Revenue Agency is desirable.

- Those who are in the process of entering in 2024, according to the Government’s Press Release, the doubling affects “individuals who transfer their tax residence to Italy, for the purposes of Article 43 of the Civil Code, after the date of entry into force.” This requires clarification. Article 43 of the Civil Code states, “The domicile of a person is in the place where they have established the main seat of their business and interests. Residence is in the place where the person has their habitual abode.” As is known from 1.1.24, the tax residence (Article 2 TUIR) has been modified and introduced a fiscal definition of domicile, so it is at least strange that the press release refers to the Civil Code and not the TUIR. In any case, we will continue to monitor the evolution of the decree, and hopefully, the Administration will release its guidelines making clarity about this item too. It is needless to underline how essential this element is for the hundreds of potential new tax residents who are deciding to move their lives to Italy in the coming weeks and months.

- Those who will enter with effect from 2025 tax year will certainly have to pay the substitute tax of 200,000 euros. The issue mentioned in point 2) above certainly applies to understand exactly when the change date is.

The Firm will continue to monitor the evolution of the “Omnibus” Decree and strive for the Administration to backtrack on this decision which, despite being entirely within the political decision-making process, is at least inappropriate in its methods and timing and and favourable to other jurisdictions. Rules should not be changed mid-course, and it would be good practice to highlight changes in advance, explaining the reasons preliminarily and, of course, being extremely clear that the changes do not affect those already within the regime.

Even with a flat tax of 200,000 euros, the Italian regime remains competitive, although it becomes more expensive for new arrivals, for the great advantages it offers in terms of international trust and wealth planning, including the use of trusts, and the absence of any “remittance” principle. The author remains available to Clients and Friends of the Firm for any further clarification. Please refer to your professional partner of reference.